RBI Policy & Its Impact on you

RBI Policy & its impact on you

The RBI surprised us by raising interest rates and it is both good and bad for us.

RBI recently did something that a lot of us were expecting but didn’t exactly see coming the way it did: it raised interest rates way ahead of its scheduled June meeting.

This surprise announcement has led to a frenzied stock market sell-off and a flurry of scary headlines.

But there’s no need to panic. Interest rate hikes are a part and parcel of life and we’re here to help you decode what exactly this means for you and the economy.

Was it long overdue ???

The first step to decoding the RBI’s interest rate hike is understanding why it was important. India had been maintaining an ultra-low interest rate (interest rates determine the cost of borrowing in the economy) of about 4% since 2018.

And this low interest rate made borrowing easy, so there was a lot of cash in the economy. Then COVID came and the financial crisis that it brought with it further prompted the government to inject extra cash into the economy. So, there was a lot of money in the economy, while the supply of goods was low, thanks to COVID.

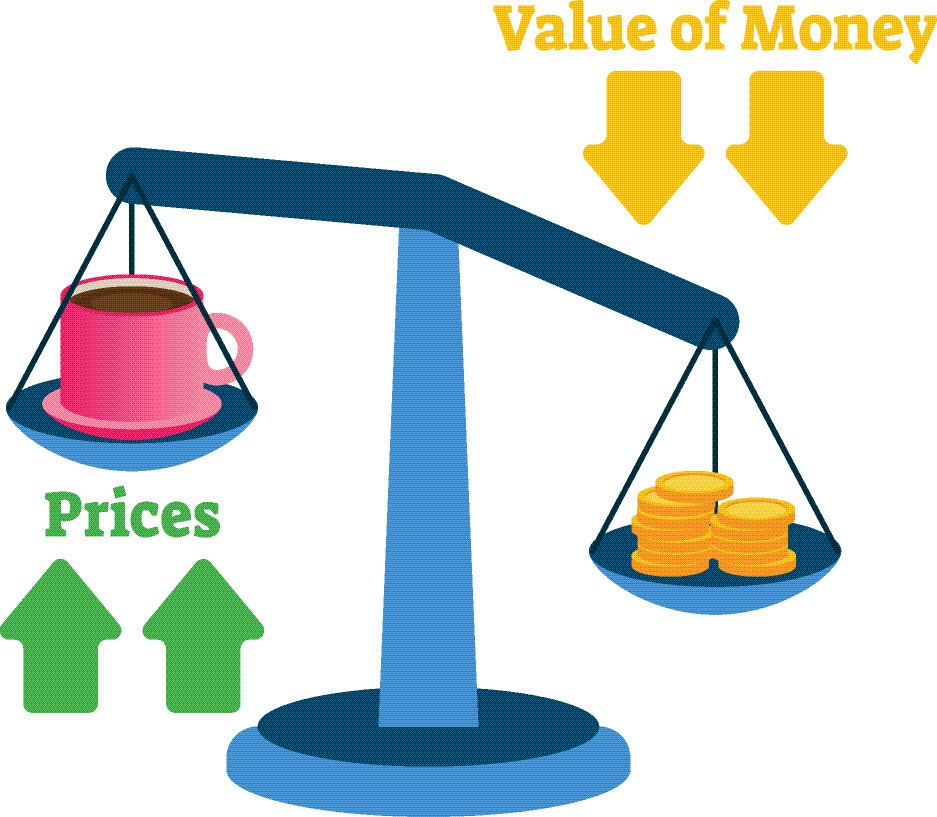

This demand-supply imbalance was the perfect recipe for inflation Add to this the tadka of the Russia-Ukraine war and Indonesia’s ban on palm oil supplies (both of which have raised the prices of commodities like grain, crude oil, and edible oil) and you get a Consumer Price Index inflation rate of 6.95% (a 17-month high).

To get this under control, the RBI has to get the amount of money in the economy under control. So, it has raised the repo rate (the cost at which it lends money to other banks) from 4% to 4.4% (this is the largest increase since 2011).

This will make it costly for banks to get money and they will pass these costs to us, making borrowing in general costlier. It is also raising the cash reserve ratio (the amount of money banks need to keep with themselves) to 4.5%. This is expected to take away Rs 87,000 Cr worth of extra money currently in the market.

So, the rate hike is a great move, no? It will bring down inflation and make goods more affordable for us again. Well, that will take some time and a few more rate hikes.

In the meantime, this rate hike can be both good and bad for you.

How will it impact your Investments

Good news first: A rise in interest rates means that this is the perfect time to invest in fixed deposits and government bonds. As interest rates rise, the rate of returns on both these instruments rises too. This kind of incentivizes people to park their money in these instruments for some time, removing the supply of this cash from the economy.

Because of this your debt mutual fund investments also pay more.

But because of the rise in interest rates, you will also have to pay more interest on your home loans, car loans, and personal loans.

Also because people are putting their money in these instruments, they sell their equity investments, causing the stock market to fall.

But are people taking money out of the stock market just because bonds give a better investment opportunity right now?….Nopes

A lot of sectors are going to suffer because of this rate hike and as a result, the stocks of these companies will also not perform that well right now.

And which are the sectors who will bear the brunt of this hike and why?

The economy, on the backfoot….

The reason why the RBI waited so long to raise the rates was that it wanted the easy money in the economy to help fuel our growth. When companies can borrow money easily, they invest in more projects, create more factories and generate employment.

But with borrowing costs high and the inflation still not tamed, many companies and industries will be in a worse situation. For instance, the automobile industry and the real estate sector will most probably see a decline in growth.

With loan rates going up, fewer people will be interested in buying houses or cars. Many automobile companies will also suffer because the cost of setting up new plants will also go up.

The telecom and infrastructure industries, which need huge funds for projects and so are heavily dependent on debt, could see a slow down in growth.

The same goes for the agricultural sector.

You see, a lot of farmers are dependent on loans to buy seeds and fertilizers. So, the rise in interest rates could become problematic for them.

Some sectors like the banking industry could see profits, while the services sector could remain unharmed.

But all in all, the economy could see a slowdown in growth and a rise in unemployment till inflation is actually tamed.

So, what should we do, right now?

Personally, we can’t do much.

Our advice: start protecting yourself from upcoming problems right now.

Create an emergency fund, and upskill yourself so that you are less likely to be impacted by the rising unemployment.

Do not take loans unless you think you will be able to bear the increased interest costs.

And most importantly, do not panic.

Related Posts

March 16, 2026

Are valuations in the stock markets getting attractive?

November 23, 2025

Rupee Meltdown vs US Dollar

October 31, 2025

Everything is very open with a clear description of the issues. It was definitely informative. Your site is extremely helpful. Thanks for sharing!

Thank you so much ☺️